We are about to enter a period of political and policy transition. As with many such transitions, there is some uncertainty. We’ll take a brief look at what may have been the most significant economic factor of the election. We’ll then shift to exploring trade policy and the implications for the US economy and capital markets.

Looking Back: Inflation

According to exit-polling, the number one issue for voters in this election cycle was the economy. Seventy-five percent of voters said that inflation had caused their family financial hardship.

Gaining a deeper understanding of voters' happiness with the state of the economy is a challenge. Research from the field of behavioral finance suggests that the rate of inflation-adjusted wage growth, relative to expectations, is what really matters.

If real income growth over time is a meaningful gauge of voter satisfaction, then the prospects for the incumbent party in the recent election were dire. Even though incomes are at an all-time high, inflation has stunted real purchasing power and left the average household below the ten-year trend of real income growth by 1%. In elections where the average household is in this position, the incumbent party nearly always loses. Going back to 1968, the only incumbent party to retain the White House when real income was below the ten-year trend by 1% or more was the Republicans, in 2004, when Bush successfully campaigned on the issue of terrorism.

Most voters are likely unaware of the ten-year trend in their own inflation-adjusted incomes. The determining factor in forming a view of the economy is far more practical. It is the dichotomy of working hard and reaching higher and higher income levels, while at the same time struggling to pay basic living expenses, all of which have increased in price substantially in recent years. When voters feel that they are keeping up their end of the bargain while the cost of living runs away from them, their view of the incumbent party tends to diminish. This conclusion is not unique to America. According to an analysis in the Financial Times, incumbent parties in developed countries worldwide all lost voter share in 2024. This is the first time in over 100 years that this has happened.

Looking Forward: Tariffs

A tariff is a tax that US firms pay to the US Treasury when they bring goods into the country from overseas. The tax can be absorbed by three parties, individually or in some combination: 1) The foreign exporting firm can accept a lower sales price, 2) The domestic importing firm can accept lower profit margins, or 3) The end consumer can pay higher prices. That’s it; there is no free lunch. Someone either pays higher prices or earns less in profit.

The Impact of Tariffs

Tariffs make imports less competitive and support domestic firms by creating a barrier to trade. The general assumption from orthodox economics has been that trade barriers lead to an inefficient allocation of resources. This is finance talk for lower overall living standards for consumers. This conclusion is true when living standards are measured by consumers’ ability to buy low-cost goods. Trade with China is great in this regard. The greater the availability of inexpensive Chinese imports, the better for consumers. However, if measuring living standards by wages and the job market, trade with China is not supportive of US consumers.

The basic framework for trade with China has been for US firms to move manufacturing jobs overseas, where the cost of labor is lower, and import those goods back home at a higher profit margin. The actual impact on the labor market in the US is significant. Manufacturing employment is only 2/3 of what it was at the end of the 1970s and 3/4 of what it was at the start of the century. To be clear, not all the job losses are from trade. Technology plays a role.

A lot of manufacturing jobs were lost in the dot-com recession and simply never came back. The recession overlaps with China joining the World Trade Organization, the group that manages trading rules and that jump-started China’s access to global markets. Even if we add in construction, another major source of blue-collar jobs, we find that employment in those two industries (21.2 million) is lower than it was at the start of the 1970s (22.2 million). It is easy to see why both political parties have an interest in resetting the terms of trade with our largest trading partner. (Labor data from Cameron Crise at Bloomberg)

Trade with China is certainly an important issue for addressing domestic economic issues, but tariffs may not be the best tool. The list of countries that have successfully used high tariffs to build up their domestic economy is worryingly short (China and South Korea), while the list of countries where high tariffs failed to improve domestic economic conditions is long (most of Latin America and Southeast Asia). That’s why so many noted economists, of the Nobel variety, have come out against the US broadly employing tariffs to improve the US economy. Historically this strategy doesn’t work very well.

The overall tariff rate on US imports moved from 1% in 2016 to now roughly 3%. Current tariffs are too small to make a perceptible difference for the aggregate economy and are too easy for Chinese firms to circumvent. For example, Chinese firms subject to US tariffs have been accused of moving final production to third party countries, mainly Mexico, or setting-up foreign subsidiaries to avoid the full impact of US tariffs. The current tariff regime is not an applicable comparison to what is being discussed now.

What’s Being Proposed?

The details here are squishy, but the general thought is that the new administration will seek to impose tariffs of up to 20% on all imports and up to 60% on Chinese exports. This is substantial and would close the loophole that China has been accused of exploiting. The last time the US imposed tariffs of 20% was under the Tariff act of 1930, which some scholars argue contributed to the severity of the Great Depression.

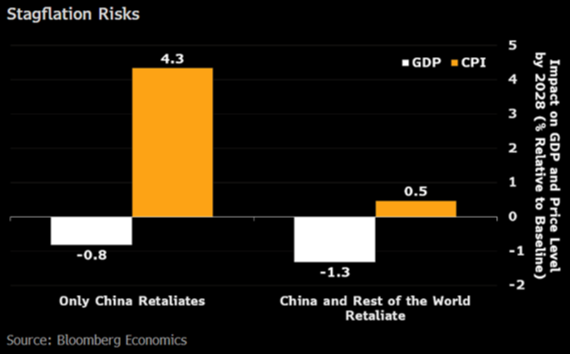

Modeling how the US economy would respond to a massive increase in tariffs is a challenge because the ultimate effect is dependent on how our trading partners and US consumers respond. Here’s Bloomberg’s view on the impact to the US economy if just China or China and the rest of the world retaliate with higher tariffs:

If only China retaliates, Bloomberg’s model shows inflation higher by 4.3%, and growth nearly 1% lower than the no tariff scenario at the end of four years. If the rest of the world joins in retaliation to US tariffs, we can expect much slower growth and a more modest increase in inflation. There are factors that could offset the impact of tariffs, such as a stronger dollar or lower taxes in the US, but the general impact will be negative. Tariffs could result in some degree of stagflation, (low growth and high inflation together), as the economy adjusts to the new trade policies. As we learned during COVID, global supply chains are too complicated to be unwound without significant complications.

The pro-tariff argument is that they will make foreign goods less competitive due to the higher prices of imports and result in the US producing more goods domestically. In theory this could bring jobs back to our shores and boost the economy. This is likely true for some, but not all, industries. If US Tariffs result in retaliation by our trading partners, the US economy would lose jobs in areas where we are currently competitive in the global marketplace (Agriculture, machinery, electronics). Bloomberg estimates that either retaliation scenario listed above would result in increased unemployment by 0.4%-0.7%. The US would lose jobs on net, and the losses would be concentrated in areas that benefit from free trade. Firms like Boeing, John Deere, Micron, and individual farmers would suffer most if easy access to foreign markets is lost due to retaliatory tariffs.

Outlook for Markets

Tariffs would add a new risk to the equity markets, and one that is not readily understood. If implemented along the proposed lines, the impact will be swift and the outcome uncertain. The result will be uneven across US equity markets. Some US firms will clearly gain from less foreign competition. Small-cap firms would benefit from higher trade barriers since they tend to be more domestically focused. Larger US firms would suffer. Apple, for example, sources 18.5% of its supply chain from Chinese facilities. How many iPhones will Apple sell if prices are significantly higher?

If US trade policy does change, the market will rotate from those firms exposed to tariff risks and into those that profit. The financial, energy and industrial sectors will likely outperform under a high tariff environment. We experienced a similar market rotation in 2022 when inflation rose to 9%. We navigated that period by moving equity and fixed income exposure into the types of investments that excel in inflationary periods.

We have argued that politics does not have the strong impact on markets that people believe. Government policies can influence the prevailing trend of the market, but they rarely change its direction on their own, outside of a rare, substantial policy change. Twenty percent tariffs, across the board, would fall into this rare and substantial category. We hope that policy makers agree and move towards more traditional trade policy strategies and negotiations.

Portfolios

The markets reacted positively to the election results, though the initial euphoria has faded. Investors are hoping that the new administration will deliver lower corporate taxes and less regulation, boosting corporate earnings. But recent market gains are less election-related and more about corporate earnings. Third quarter S&P 500 earnings were twice as strong as forecasted, and forward guidance for 2025 earnings has been moving higher since before the election. Equity market fundamentals are strong, even if campaign promises don’t materialize.

All this may seem somewhat contradictory. Broad-based tariffs may increase inflation, slow growth and hinder the job market, but lower taxes and fewer regulations may be supportive of corporate earnings and stock prices. Can all this be true at the same time? Maybe yes. The extent to which proposed and assumed economic policy changes actually come to fruition can’t be known. And consumers and capital markets typically adapt to changing conditions. No policymaker wants to initiate a recession (unless in extreme circumstances such as high inflation) or a bear market, regardless of political persuasion.

We are not making any election-related portfolio changes, though a rebalance will be coming shortly. We anticipate that equity markets will remain strong through year-end. Any significant policy changes from Washington are still months away. We will remain attuned to developments.

Closing Comments

With the holiday season once again upon us, we wish to express our sincere gratitude for the opportunity to serve each and every one of you. It is an honor and responsibility that we take most seriously and for which we are most grateful.

From our families to yours, our very best wishes for a happy and peaceful season.